Earnings Growth: Deceleration but Continued Expansion

- The estimated year-over-year earnings growth rate for the S&P 500 in Q2 2025 stands at 4.9%. This represents a notable slowdown from the robust 11.9% growth recorded in Q1 2025.

- If this estimate holds, it would be the lowest growth rate since Q4 2023 (4.0%).

- Revenue growth is also moderating, with an estimated 4.1% year-over-year increase, below both the 5-year (7.0%) and 10-year (5.2%) averages.

- This would mark the 19th consecutive quarter of revenue growth for the index.

Earnings Revisions: Widespread Downward Adjustments

- Since the start of Q2, analysts have reduced earnings estimates for S&P 500 companies by 4.1% on a per-share basis—more than the 5-year (-3.0%) and 10-year (-3.1%) averages for estimate cuts within a quarter.

- Downward revisions have been broad-based, affecting 14 of 16 tracked sectors, with only Aerospace and Utilities seeing estimate increases.

- The largest cuts have hit Conglomerates, Autos, Transportation, Energy, Basic Materials, and Construction.

- Even the pivotal Technology and Finance sectors, which together account for over half of S&P 500 earnings, have seen estimates revised down, though the pace of cuts in Tech has stabilized recently.

Corporate Guidance: Mixed Signals

- For Q2 2025, 58 S&P 500 companies have issued negative EPS guidance, while 50 have issued positive guidance.

- The proportion of negative guidance is actually less than average, suggesting that while expectations have moderated, outright pessimism is not widespread.

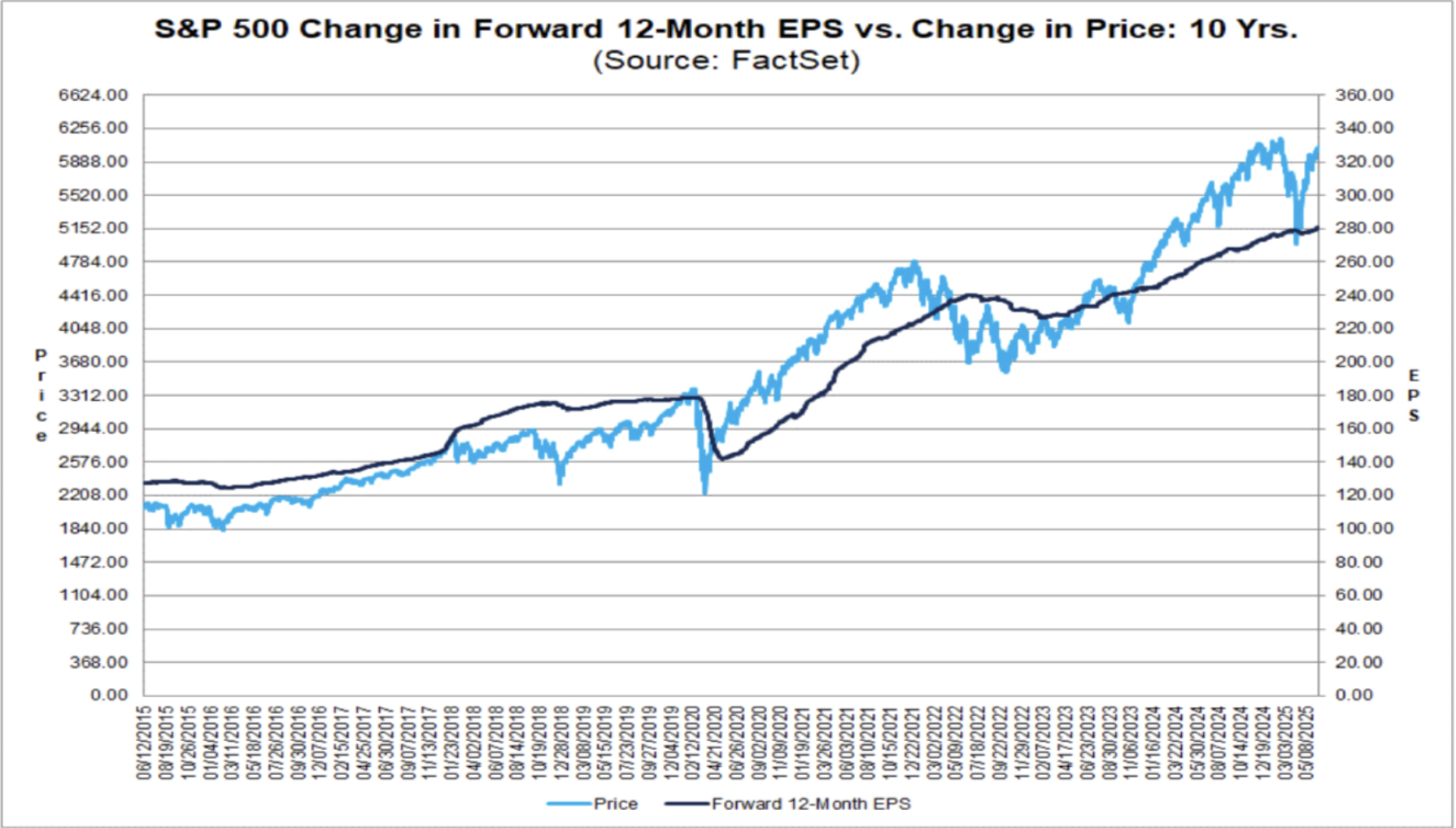

Valuations: Elevated Relative to History

- The forward 12-month price-to-earnings (P/E) ratio for the S&P 500 is 21.6, above both the 5-year (19.9) and 10-year (18.4) averages.

- This elevated valuation persists despite the deceleration in earnings growth, reflecting continued investor optimism or a premium for perceived quality and resilience.

Sector and Company Highlights

- Information Technology: This sector continues to lead, with all six industries projected to report year-over-year revenue growth, and the sector as a whole expected to post the highest revenue growth rate at 11.8%.

- Example: Broadcom (AVGO) reported a standout quarter with 20% total revenue growth, driven by a 46% surge in AI semiconductor revenue and successful software integration.

- Energy: The only sector expected to report a year-over-year decline in revenues, reflecting ongoing challenges from lower energy prices and weaker product margins.

- Consumer and Services: Companies like Disney and Starbucks have reported solid results, with Disney posting a 7% revenue increase and Starbucks seeing a 2% rise in consolidated net revenues, though both have faced margin pressures from higher costs and strategic investments.

Market Sentiment and Outlook

- The Q2 earnings season is occurring against a backdrop of heightened market volatility and shifting investor sentiment, influenced by macroeconomic uncertainty and global trade dynamics.

- The rotation from growth to value stocks observed in Q1 has continued, with value and dividend strategies outperforming, and international equities gaining traction as investors seek diversification.

- Despite the moderation in earnings growth, corporate results have largely exceeded lowered expectations, helping to support equity market rebounds and maintain elevated valuations.

Conclusion

The Q2 2025 earnings season is marked by a clear deceleration in both earnings and revenue growth for the S&P 500, with widespread downward revisions to estimates and sector-specific headwinds, particularly in Energy and cyclicals. However, the resilience of key sectors like Technology, the stabilization of estimate cuts, and a less-than-average share of negative guidance suggest that the corporate profit engine remains intact, albeit at a slower pace. Elevated valuations and ongoing macroeconomic uncertainty warrant vigilance, but the overall tone of the season so far is one of cautious optimism, supported by robust results from industry leaders and persistent revenue growth across most sectors.

Disclaimer

The information provided on this website is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. The content, including any analytics, commentary, opinions, or data, is not intended as a recommendation to buy, sell, or hold any security or investment strategy. All investments in equities and other financial instruments involve significant risk, including the potential loss of your entire investment.

Past performance is not indicative of future results. The value of investments can go down as well as up, and there is no guarantee that any investment strategy will achieve its objectives or that any information provided will result in profits or prevent losses. The analysis and opinions expressed on this website are based on publicly available information and sources believed to be reliable, but we do not guarantee their accuracy, completeness, or timeliness.

We are not registered investment advisors, brokers, or dealers. You should not rely solely on the information provided here to make investment decisions. Before making any investment, you should conduct your own research and due diligence, and consult with a qualified financial advisor or other professional who is familiar with your individual circumstances and objectives.

By using this website, you acknowledge and agree that you are solely responsible for your own investment decisions and that the website and its contributors are not liable for any losses or damages arising from your use of the information provided.